President Joe Biden has a long, well-documented history of telling tall tales. Accordingly, it was not a surprise that his State of the Union address Feb. 7 included many misleading and inaccurate claims.

Although a group of experts dissected the speech in real time, one line in particular is worth rebutting at length:

In the last two years, my administration has cut the deficit by more than $1.7 trillion—the largest deficit reduction in American history.

With the national debt and federal spending set to be a pivotal political battle this year, understanding the truth about Biden’s fiscal record is vital.

The deficit for fiscal year 2020 was a record $3.1 trillion. There’s no mystery about why: Lower tax revenue due to pandemic lockdowns reducing economic activity combined with increased spending (much of it wasted) meant the year was a perfect storm for adding to the national debt.

Although some pandemic-related restrictions lingered, the end of lockdowns meant the economy (and tax revenue) largely bounced back in fiscal year 2021—and this would have happened regardless of who was president. Similarly, the bulk of stimulus spending enacted in 2020 wasn’t designed to carry over into future years, meaning that federal spending was expected to dip in 2021.

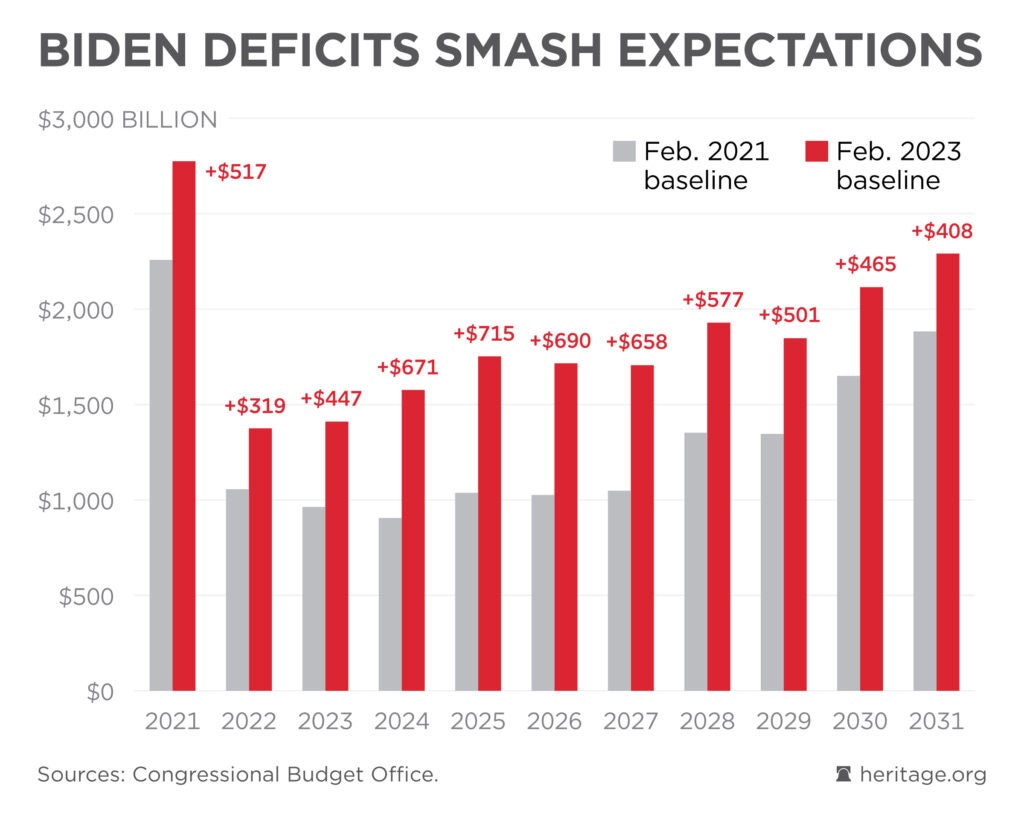

Because of those factors, the Congressional Budget Office predicted that the federal deficit would decline sharply between fiscal years 2020 and 2022.

However, an updated report from the CBO reveals that the deficit Biden has been bragging about was actually $319 billion higher than what was expected when he had just taken office on Jan. 20, 2021.

In fact, deficits through fiscal year 2031 are on pace to total a staggering $6 trillion more than when the Biden administration began, or about $46,000 for every household in the country.

This isn’t an accident, but instead the result of many deliberate choices by Biden and Congress to increase spending and add to the national debt recklessly. Here are seven:

- The largest by far was the $1.9 trillion package of welfare expansions and bailouts in March 2021, which passed Congress with Democrat-only support. It was promoted as a response to COVID-19. In reality, the bill was a textbook example of political opportunism that took advantage of the pandemic to enact a raft of the Left’s priorities.

- The 2021 infrastructure package, which Biden regularly cites as an achievement, was loaded with budget gimmicks to hide its true cost and included many wasteful carve-outs for progressives. The Biden administration’s highly flawed and partisan implementation of the bill only has made things worse.

- Biden was happy to sign two omnibus appropriations packages, both of which were thousands of pages long, larded up with pork and unnecessary spending increases for the swamp, and included tens of billions in questionable non-military aid to Ukraine.

- The so-called Inflation Reduction Act, a mix of tax hikes and Green New Deal-style industrial subsidies, was designed in a way that will add to deficits over the first five years and add even more down the line if any of its spending is renewed. Incredibly, things would have been even worse if the originally planned “Build Back Better” debacle had become law.

- The COMPETES Act, supposedly about addressing challenges posed by China, was in fact a deficit-financed mess of corporate welfare and increased spending authorizations for federal “science” bureaucracies.

- The PACT Act started as a reasonable measure to assist veterans who suffered from toxic exposure, but was turned into a massive expansion for the government-run Veterans Affairs system with a huge price tag. Since veterans’ benefits are a core federal responsibility, Congress should have the decency to ensure the VA system is paid for rather than casually swiping the national credit card.

- Biden has enacted or is in the process of implementing several executive orders and regulations that add billions of dollars apiece to costs, leading to a mix of higher deficits and reduced purchasing power. These include a massive “Thrifty Food Plan” increase in food stamp benefits; college loan repayment deferrals and the still-pending forgiveness scheme; an Obamacare eligibility expansion; and more stringent rules for two types of labor mandates on infrastructure projects.

This continual surge of deficit spending was a leading factor in the surge of inflation, leading the Federal Reserve to start hiking interest rates, a development that could stall the economic recovery.

During his State of the Union speech, Biden blamed the high national debt on the Trump administration. This deflection has a kernel of truth—deficits were too high from 2017 through 2020—but removes all context. The bulk of Trump-era deficit increases were the result of bipartisan spending bills such as the CARES Act of March 2020 and excessively large appropriations packages.

Democrats also attempt to blame deficits on the 2017 tax cut, but tax revenues now actually exceeded projections made before that bill’s passage and in 2022 were at a multidecade high as a share of the economy.

The bottom line is that the debt is too high, the long-term budget outlook is dismal, and both parties recklessly have made this problem worse over the past 20 years. Accordingly, both parties need to take the issue seriously and prioritize the nation’s financial health.

A good place for legislators to start is The Heritage Foundation’s Budget Blueprint, which provides comprehensive guidance across the spectrum of policy issues. (The Daily Signal is Heritage’s multimedia news organization.)

The Budget Blueprint contains $15.5 trillion in spending reductions, along with trillions of dollars in improvements to the tax code. Although many of the proposals are unlikely to occur while Democrats control the Senate and the White House, even a fraction of that amount would be a huge first step toward digging out of the enormous hole we’re in.

The alternative—ignoring the problem and prioritizing short-term political calculations—invites more waves of punishing inflation and debilitating interest rate hikes.

This is a time for leadership. And if policymakers in Washington won’t lead, it will be up to the American people to hold them accountable.

Have an opinion about this article? To sound off, please email letters@DailySignal.com and we’ll consider publishing your edited remarks in our regular “We Hear You” feature. Remember to include the url or headline of the article plus your name and town and/or state.