As his father sailed before him, and his son marches behind him, Stephen M. Calk Sr. served America in uniform. He was a U.S. Army helicopter pilot. Amid a highly successful banking career, Calk aspired to serve his country again as a top national-security official or diplomat.

This patriotic commitment bought Calk five and a half months behind bars, $1.25 million in fines, and $17.2 million in legal bills. Federal prosecutors turned his bank’s über-collateralized loan to campaign consultant Paul Manafort into Calk’s personal Highway to Hell. If you wonder what lawfare looks like, keep reading.

Between his honorable discharge as an Army captain in February 2001 and the start of his jaw-dropping battle with weaponized federal injustice, Calk was founder and CEO of The Federal Savings Bank. This Chicago-based institution chiefly supplies mortgages and refinancing to active-duty military personnel, veterans, and new homeowners.

“From 2011 to 2019, I built this platform, so we could do business in every state of the union,” Calk told me at his residence in Naples, Florida. “We literally could do this 24/7/365. Whenever soldiers, sailors, and airmen needed us, we would be there.”

“Steve ensured that his team took care of all our needs as first-time home buyers,” recalls retired Marine Lt. Col. Darin Lierly. The Fresno, California-based pilot with a major U.S. airline met Calk in 1986 at Fort Rucker, Alabama’s Army Flight Training School. “I would have likely ended up in a financial bind for many years had TFSB not secured an affordable, responsible mortgage for us.”

But for all of Calk’s loyalty and compassion, one former customer suggests that he does not cut corners.

“If Steve and I were in a foxhole together, and a grenade flew in, we would probably kill each other fighting to see who would cover it first,” said Army National Guard Chief Warrant Officer 4 William R. Sinton, a retired aviator who met Calk 40 years ago, as a fellow pilot trainee.

As Sinton eyed a vacation home on Chesapeake Bay, “Steve stepped in and explained the workings of his bank, and how he could help,” Sinton reminisced. “At first, I just casually filled out the loan documents, thinking it was just a formality with Steve at the helm.”

Sinton should have taken this process as seriously as Calk did.

“Steve called me and reminded me that my lack of detail and clarity in my application would not fly with his loan officers, and that I must get my ducks in a row, do my due diligence, and file a thorough and detailed mortgage application,” Sinton continued. “If not, his loan officers would deny it, and Steve would concur.”

As Calk kept banking, Donald Trump began running for president in 2016. Calk became an early supporter. Trump’s campaign named him one of the “Six Steves” (along with Feinberg, Miller, Mnuchin, Moore, and Roth) who advised the Republican candidate on public policy and sold his program to voters.

Calk was a “super surrogate” who appeared in about three dozen interviews and promoted the America First vision to journalists in the “spin rooms” after all three presidential debates between Trump and Democrat nominee Hillary Clinton.

After Trump crushed Clinton in an upset victory, Calk hoped to assist the incoming president. He considered himself suitably educated and experienced to serve as secretary or undersecretary of the Army or U.S. ambassador to England, France, or Germany.

He felt quite comfortable in Europe. “I grew up in Great Britain and learned French there,” Calk said. His U.S. Navy veteran father was an expatriate executive with the Playtex Corporation during the family’s nearly six years in London. “It would not have taken much time to brush up my French skills.”

Several Trump aides backed Calk, not least former campaign chief Manafort, and then-ally Anthony Scaramucci. On Jan. 9, 2017, the transition team asked Calk to travel the very next morning from Chicago to Manhattan for a hastily scheduled pre-screening interview at Trump Tower. Calk booked a last-minute American Airlines flight for approximately $1,000, between O’Hare and LaGuardia airports, and he stayed overnight at the Four Seasons Hotel for about $600.

Calk never got hired for a Trump-45 post. Regardless, the Empire struck back.

Unfortunately for Calk, his roughly $1,600 in travel expenses exceeded the $1,000 threshold that triggers 18 U.S. Code § 215, the federal bank bribery statute. He believes that his high-profile TV segments made him a target of Trump-hating federal prosecutors.

“It is my understanding that in their desperate attempt to smear President Trump, they came across my name while investigating Paul Manafort,” Calk fumed. “They then completely fabricated the concept that Manafort’s TFSB loan was ‘risky.’”

Deep state careerists at the Justice Department cooked up what they dubbed Calk’s “corrupt scheme.” They argued outlandishly that Manafort’s cost-free employment recommendation was a “thing of value” equal to Calk’s $1,600 job-interview travel costs. Even though Calk paid this money, the Justice Department conflated it with Manafort’s referral to create a “bribe” to entice Calk’s approval of what the DOJ called Manafort’s “high-risk loans.”

Even by DOJ’s pretzel logic, this case made zero sense.

Bribes to bankers usually pour into their pockets. This “crime’s” pivotal $1,600 flowed out of Calk’s pocket to cover his own travel outlays. DOJ prosecuted Calk for bribing himself.

Manafort’s endorsement of Calk bore no price tag. Human beings routinely advocate capable colleagues, associates, and loved ones for employment. This happens worldwide, daily, for free.

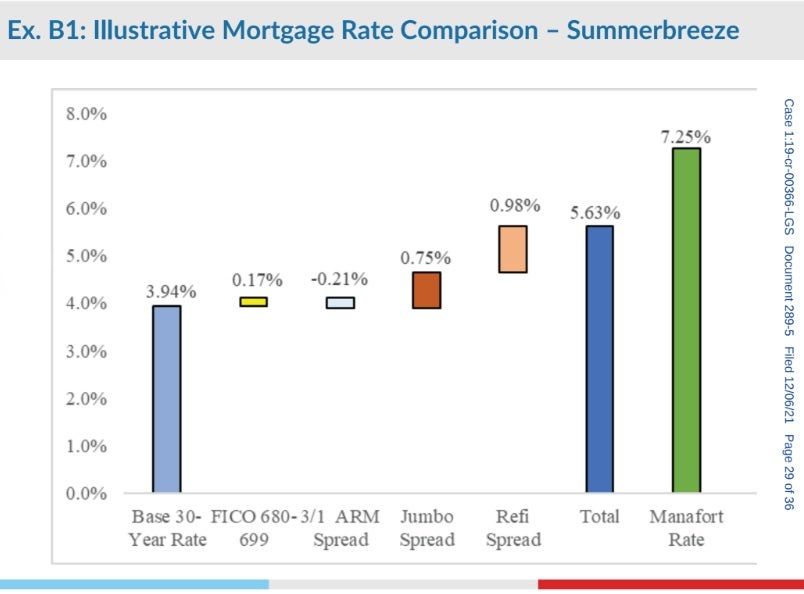

TFSB’s loans to Manafort were as risky as betting on the exact time that the Sun will set this evening into the Gulf of America. According to Calk’s April 19, 2024 petition for the U.S. Supreme Court to review his case, “the loans were made on standard terms (or better for TFSB), were approved by the underwriting department, and were supported by so much collateral that they posed effectively no risk to the bank.” (SCOTUS denied Calk’s petition.)

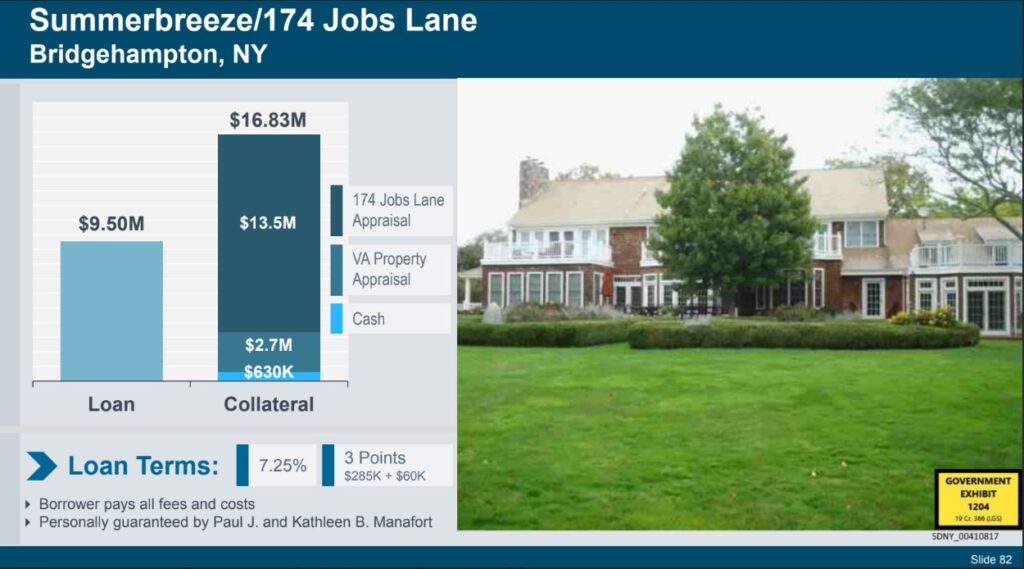

TFSB’s $16 million loan to Manafort was over-collateralized by $25 million in real estate. “I personally inspected Manafort’s home in the Hamptons, to make sure it was worth what he claimed,” Calk said. TFSB charged Manafort 7.25% interest, “just like every other portfolio loan we wrote,” Calk specified, plus an additional 3%. “Manafort paid the standard fees, points, appraisal costs, and all else. He got absolutely no favorable treatment.”

TFSB disbursed just $8 million of the $16 million loan. After Manafort succumbed to his own legal woes, the DOJ seized his assets, and Manafort defaulted on this debt. TFSB spent a year suing the DOJ to recover the property. When the bank prevailed and repossessed Manafort’s estate, its doors were not just unlocked. They were wide open. The mansion was infested by pests and marred by rain and snow.

“The house sustained significant damage because of the feds’ neglect,” Calk recollects. “All of the gardens were overgrown, and tree limbs and branches were strewn about the unattended lawn and gardens.”

Nevertheless, Calk explained, “The bank did not lose one single penny.” It recovered “100% of principal, interest, fees, and penalties. Therefore, it became the single most profitable loan in the bank’s history.

“In hindsight, there was zero risk in extending this loan to Manafort. It was the best-collateralized loan in the bank’s history, with cash and millions of dollars of mortgage-free real estate: A mansion in Bridgehampton, New York; a luxury condominium on the Potomac in Old Alexandria, Virginia; and a stunning brownstone in Carroll Gardens, Brooklyn. Beyond real estate worth more than the loan itself, the bank held Manafort’s cash accounts worth $2.5 million in additional collateral, out of an abundance of caution. We held a ton of cash in the bank, with a brick on it.”

Despite these exculpatory facts, President Joe Biden’s DOJ continued this cruel, unusual case.

“I asked my lawyers, ‘Did I cross a line somewhere?’ If so, I would have pleaded guilty to a misdemeanor,” Calk frowned. “But I was not going to plead guilty, because I did nothing wrong.”

Calk surrendered at federal court in Manhattan on May 23, 2019. He grimly described being slapped into handcuffs and leg irons before his jailers took his mugshots and fingerprints. “After all of my service to this country, the family I raised, and the business I built, I could not believe I was in that position,” Calk lamented.

Calk vividly remembers one facet of his federal trial, which COVID-19 delayed until June 22, 2021. “As soon as the Manhattan jury heard that I supported President Trump, you could see them stir with discomfort.” The U.S. courthouse’s bipolar heating and cooling system baked and froze jurors as they struggled to absorb arid testimony about property valuations, lending protocols, corporate governance, and other arcana.

After three weeks in court, the jury convicted Calk on July 13, 2021.

“Calk used the federally-insured bank he ran as his personal piggy bank to try and buy himself prestige and power,” then-U.S. Attorney for the Southern District of New York Audrey Strauss claimed, after the verdict.

“Audrey Strauss’ response is absolutely outrageous!” Calk seethed. “I have forgotten more about safe and sound banking and lending risk than Ms. Strauss and her corrupt prosecutors will ever know.”

“My persecution and prosecution were clearly an attempt to smear President Trump and detract from the great work of his first administration,” Calk added. “My decision to fight back and refuse to negotiate a lesser charge or admit guilt to a crime I never committed, all at great personal expense, was and is the right thing to do. How could I ever look into the eyes of my children, my family, or the hundreds of soldiers, sailors, airmen, and Marines whom I have supported, if I were not willing to fight this corruption and these lies?”

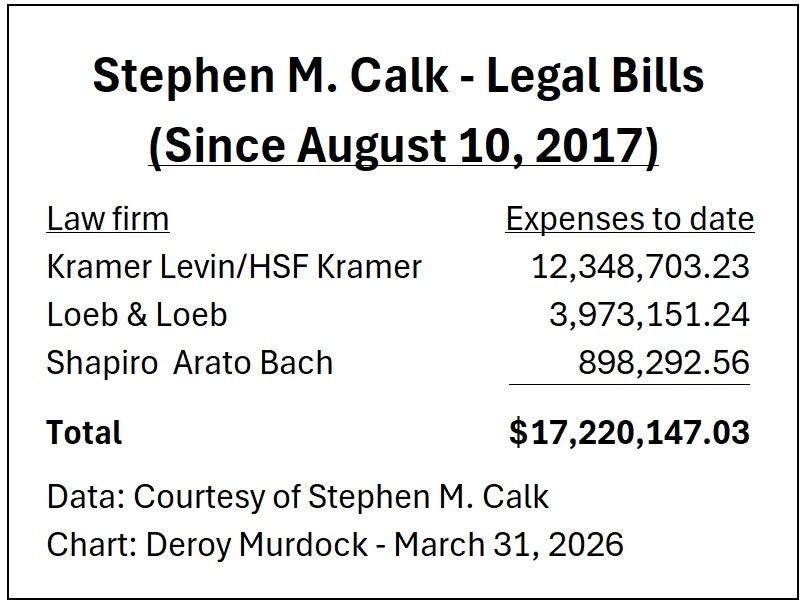

Calk has suffered $1.25 million in fines, five and a half months (of a 366-day sentence) at the Federal Prison Camp in Duluth, Minnesota; two months at a Salvation Army halfway house in Fort Myers, Florida (while wearing an ankle monitor), and one month of home confinement. To date, Calk’s legal bills total $17,220,147.03. With that sum, he could purchase median family homes at $405,330 each and donate them to 42 veterans, their spouses, and children.

Calk also saw a Visa credit card canceled after more than 30 years. His USAA homeowner’s insurance plan, TSA Global Entry membership, and gun permits were all canceled.

“Citibank, JPMorgan Chase, and American Express de-banked me,” Calk grieved. “I was also kicked out of all my business and social clubs. The reputational damage can never be repaired.”

This ordeal’s opportunity cost has been enormous—for Calk, his colleagues, and their customers. At its 2020 peak, TFSB’s 2,200 employees managed $11 billion in annual loan volume. Calk estimates that had he not endured this nonsense since August 2017, TFSB today would have 5,000 staffers overseeing $50 billion in mortgages. Instead, TFSB’s payroll has shriveled to 1,500 people—down 31.8% since TFSB’s zenith in 2020. They oversaw just $3.5 billion in loans last year—down 68.2%.

“How many more people could we have helped?” Calk sighed. “It’s staggering.”

While Americans—GIs, veterans, and civilians—hunger for affordable housing, TFSB shrinks.

“I had been the driving force of all of TFSB’s growth, recruiting, strategic planning, and hiring of key personnel,” Calk stated. “Now, I can’t work at the bank. I can’t walk in. I cannot even call the bank. It totally lacks my leadership.”

Worst of all, because Calk’s beloved brother John (a retired U.S. Army first lieutenant and armor officer) has equity in TFSB, the federal government forbids them to discuss business. So, to be safe, they simply do not speak.

Calk’s torture is relentless. Because of his conviction, the Federal Reserve Board could seize TSFB, place it in a blind trust, and force its fire sale. His entire career’s work could go up in smoke at any moment, and he lives minute by minute, worried that the Fed might strike that match.

There is a way out: Stephen M. Calk Sr.’s fully vetted and widely supported pardon papers can be placed on the Resolute Desk at any time. This bizarre, twisted injustice finally could end via the big, beautiful signature of President Donald Trump.

We publish a variety of perspectives. Nothing written here is to be construed as representing the views of The Daily Signal.