Americans have felt the effects of ballooning inflation as a direct result of government-mandated shutdowns of the economy. Prices on essential goods, including food and gas, have risen steadily over the past few months, leaving many wondering about the economic health of the nation.

“This past year and a half, we also saw a very sharp economic decline, larger in a single quarter than we have seen in any of our lifetimes, unless you were around back in the 1930s,” says Joel Griffith, research fellow in financial regulations at The Heritage Foundation.

Griffith joins us today on “The Daily Signal Podcast” to talk about the latest inflation numbers and how good fiscal policy can help us right the ship.

We also cover these news stories:

- The Taliban capture the strategically significant cities of Ghazni and Herat, marking the fall of 11 out of 34 provincial capitals after a weeklong blitz of fighting.

- Texas Gov. Greg Abbott and state Attorney General Ken Paxton push back on Dallas County’s new mask mandate.

- A recent report details how Oregon Gov. Kate Brown quietly signed into law a measure ending graduation requirements for students to prove they can read, write, and do math at a high school level.

- New York Gov. Andrew Cuomo is going to step down, but Republicans and Democrats alike call for him to be held accountable for his handling of nursing homes during the COVID-19 pandemic.

Listen to the podcast below or read the lightly edited transcript.

Doug Blair: Our guest today is Joel Griffith, a research fellow in The Heritage Foundation’s Roe Institute for Economic Policy. Joel, welcome to the show.

TRENDING ARTICLES

Joel Griffith: Hey, hello. Thanks for having me today. Good to be here.

Blair: Great, awesome. So, there’s been a lot of talk in the news recently about high inflation and what impact it’s having on the American financial situation, right? So can you explain exactly to us what high inflation means and what the effects are on the economy?

Griffith: Yeah. When we talk about inflation overall, what we mean is the overall price level, rather than any one particular item that you might be buying.

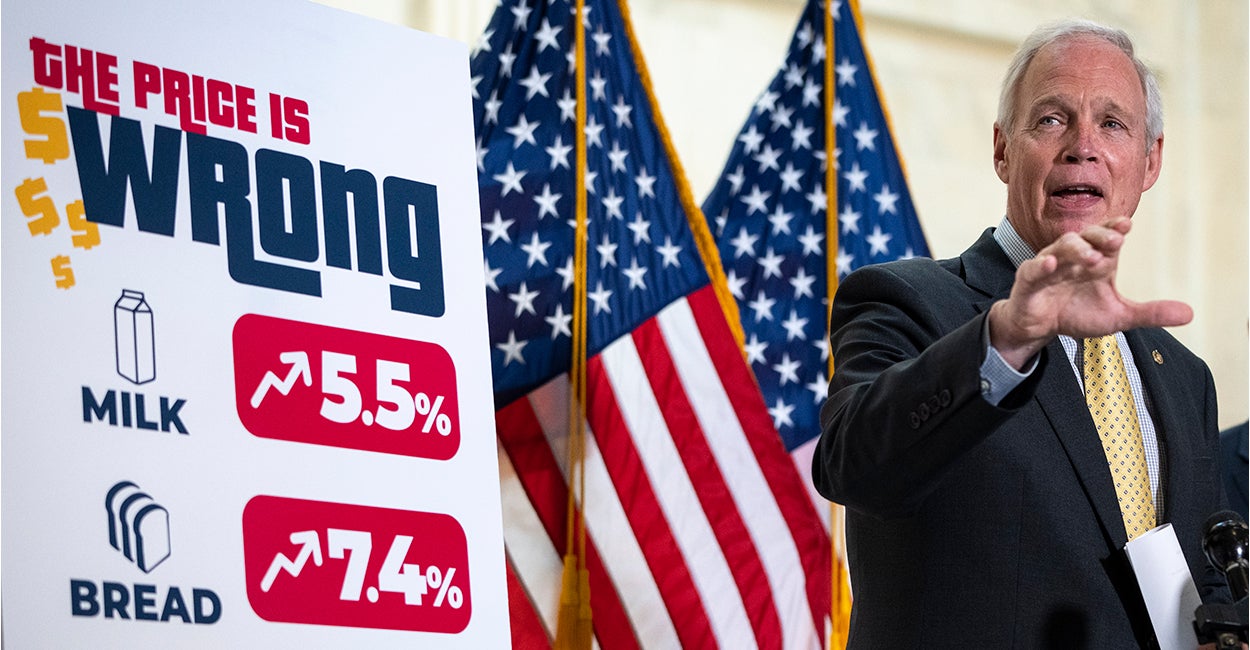

Now, of course, a lot of us have noticed over the past year, it is costing us noticeably more to fill up our vehicles. Energy prices are up about 40% year over year, and there’s a lot of food items too. There’s a number of items. We talk about inflation, we’re talking about the overall increase in the price level, and that too actually has been dramatically higher than what we’ve been used to over many years.

Just today, the new numbers came out for the month of July, prices rose overall by 0.5% in just one month alone. And year over year, we’re looking at increases that are 5.4% higher year over year. And that is the highest, it’s going back to 2008. So for a lot of people that have entered the jobs market in the past decade, they have never experienced a year in which prices overall have increased by this much.

Blair: Now, you mentioned 2008. And obviously, a lot of our listeners, that’s going to probably bring back some pretty negative memories of like, “Wow, my economic situation was horrendous at that time.” Are we saying that now the current economic health of the country is similar to 2008? Or is it worse? Is it better? Where are we at?

Griffith: Back in 2008, 2009 era, that was one of the worst economic downturns we have seen since the Great Depression, which was in the 1930s. In the 2008 era, that was when housing prices collapsed. We had a stock market collapse. We had … many big banks that went under.

Now, this situation that we’re dealing with right now is quite a bit different.

This past year and a half, we also saw a very sharp economic decline, larger in a single quarter than we have seen in any of our lifetimes, unless you were around back in the 1930s. But that was an economic collapse this past year caused by governmental response to COVID-19, the first time in our nation’s history where we actually saw governments intentionally suppress economic activity.

And because of the nature of that economic collapse that we saw a year and a half ago, the rebound has been very, very sharp, on the upside. Because once government said, “All right, you can go back to work, you can resume your lives,” we saw the economy snap back.

So in many ways, the economy now that we’re experiencing is actually much better for most people than it was in the recession before, which is more than a decade ago.

Blair: Sure. So, it sounds almost like what you’re saying is that a lot of the current economic situation is tied more to efforts made by the government and government bodies, as opposed to the pandemic itself, is that accurate?

Griffith: And that really plays out across the United States because unlike pretty much every other developed country in the world, we have a federalist system, meaning that each of our 50 states has quite a bit of power to determine their own economic policy.

So over the past year and a half, you had some states that were shut down just for two weeks to three weeks, like Florida, that rapidly reopened. And meanwhile, you had places like New York, and Michigan, and California that kept much of their economy shuttered for the better part of a year. And now the data started really showing the difference in economic output by state.

You have a dozen states or so that have bigger economies now than they did before the pandemic. But you have places like Hawaii, New York, and California that are still quite a bit smaller and still have a higher unemployment than they did prior to the pandemic.

Blair: Sure. So, going back to what you mentioned earlier at the beginning of the interview, you mentioned that July inflation numbers actually just released. I have some of the data in front of me right now. They said the core inflation rose about 3% while the consumer price index rose 5.4% from last year. Having these numbers in our hands, what does that tell us about the direction the economy is heading, coming from data from last month or from early in the year?

Griffith: Yeah. Well, a number of these items really reflect the rapid reopening of the economy. If you look at energy costs, for instance, that’s the biggest increase year over year, has been an energy overall. And that’s in large part because the economy reopened in some ways faster than some of the experts and some of the energy producers predicted.

So as you saw travel surge, for instance, airline travel, people just driving, manufacturing overall, it caught some of those producers off footed. So we have seen supply outpace demand growth, and we’ve seen a surge in those prices.

If you look at vehicle prices—I’m one of those who actually bought a used vehicle earlier this year. It’s not in your imagination. Used car prices are up 40% in just the past year. Many people are finding that they bought a vehicle four or five months ago and they’re finding their used car value has actually increased in value despite the norm of it going down fairly steadily over time. Well, that in part is because we’re flush with a lot of extra cash. But also, we have a microchip problem, where we have a shortage. So it’s much more difficult to find a new car at a comparable price.

So everything is really interrelated here. It’s hard to put your finger on any one cause, but we know the reopening, the supply chain issues, and then our own government’s mismanagement of the monetary system, that is also partially to blame for this unusually large increase in prices.

Blair: Now, I’m curious, because we see all these products, like you mentioned, obviously, used cars and other kind of items that people generally buy on a daily basis are becoming more expensive. How does this affect a paycheck? How does this affect somebody’s wages? Is there any effect that this inflation has on people’s actual money?

Griffith: When you see inflation and the overall price level increasing faster than someone’s salary growth, which is what we have seen lately, well, that means that your real wages, they purchase less.

And that’s one of the concerns really longer term, is even if this burst of inflation proves to be temporary, that the rate of inflation, let’s say this 5% rate, will come back down to the typical average that we’ve seen over the longer term of, say, 2% per year. Well, if your salary this past year, your wages only increased 2% and your cost of living increased 5%, even if inflation comes back down to that 2% long-term average, if your income growth only continues at its historical rate of growth, well, that means that you have permanently seen a 3% decline in your income relative to where you would have been were it not for this surge of inflation.

Blair: So you’re basically saying that you could be making the same amount of money as you were before, but due to inflation and due to the fact that this level of inflation that we’re seeing right now is so severe, you in effect are taking a pay cut?

Griffith: Right. Even if this is—a lot of economists are using the word “transitory” to refer to this inflation burst, suggesting that it’ll come back to normal, that inflation will return to its historical norm. The problem is, if you never make up for that gap in terms of your wages, then that could be a permanent reduction in your real wages for years to come.

Blair: Wow. That sounds like a big issue. On that sort of similar topic of wages and work, another topic that’s been popping up a lot recently in the news is the job market. We also got some relatively recent numbers on the American labor market, and it shows that there are around 10 million open jobs in the country currently. Now, that seems like a lot of jobs, but there’s also reporting that indicates that unemployment is huge as well. So I guess, how does that mesh, like, how do we have such high unemployment when there seems to be so many jobs out there?

Griffith: Well, we lost many jobs, of course, during the shutdown. And in some areas of the country, thanks to the reopening, we actually do see unemployment rates that are as low or lower than they were prior to the pandemic.

In fact, as you just referenced, the number of job openings we have now is actually at an all-time record high. For a number of months now, we’ve had an all-time record high of job openings. We have more job openings now than we did prior to the pandemic. We have more job openings than we do people looking for work.

And we have a situation that in our small business sector, nearly half of all businesses that participated in a recent [National Federation of Independent Business] survey reported that they’re having problems, staffing. And if you go to any town or city across America, you’ll probably see this as well.

I was with family recently in South Carolina, and most of the bars and restaurants had “help wanted” signs. Many of them had limited their hours or their seating, not because of COVID—they’re over those restrictions in South Carolina—it’s because they cannot find staff.

Well, in this instance, government has actually caused a big part of this problem. And that’s because we are paying people. Thanks to a federal unemployment bonus, many people have found they can “earn” more … not working than working. And because of that, many people have chosen to simply stay home. It’s a big part of why we actually have a labor shortage right now.

And once again, the data confirm this, is we have a number of states—I think two dozen states now—that have said, “We are no longer going to accept these federal unemployment benefits.” And it just so happens that it’s most of those states that are ahead of the pack in terms of getting their unemployment rates down. But that’s because people have been incentivized to go back to work because they can no longer take in those enormous federal unemployment bonuses.

Blair: It sounds like, basically, the biggest issue here is bad fiscal policy. I’m curious then, Joel, what is the role of government in terms of fiscal policy? I mean, does Congress have a role in controlling inflation? Does it have a role in doing these types of things? Where does the government step in?

Griffith: Well, Congress has the ultimate power of the purse to actually appropriate and spend and tax. And unfortunately, both Republicans and Democrats, for many years now, have not acted prudently. It’s why nearly each and every year, actually, each and every year, since the era of President Bill Clinton and [House] Speaker Newt Gingrich back in the early ’90s, each and every year, we’ve actually run a deficit. And in the last few years, those deficits have gotten wider and wider.

And we’re fortunate we live in a free market economy where we do have quite a bit of economic freedom. So, we’ve still achieved productivity gains. We’ve still been able to see families earn more over time. But it could’ve been so much better because we’ve seen the government gobble up more and more of our resources. And it’s gotten far, far worse over the past year and a half throughout COVID.

Blair: Right. So now that we have this sort of idea of the government has this role in matters of fiscal policy, and this is what they should be doing, where should our listeners go if they want to learn a little bit more about fiscal policy we want to be seeing from our government?

Griffith: Well, here at The Heritage Foundation, if you go to heritage.org, any type of issue that you’re interested in, you can just put it in the search bar and it’ll pop up. And of course, we also are very active on Twitter, just staying up with current events.

But these are very important issues. And we have seen so much happen over the last year and a half with politicians using COVID as an excuse to embark on wild spending programs under the guise of helping us through the crisis. But we know what can get us through this crisis. It’s allowing people to go back to work. And in states where that has happened, people are actually enjoying their lives again. We see the economy’s booming again.

And unfortunately, a lot of what we see in terms of legislation continues to suggest that we’re in this state of emergency in which we need massive government help. Just look at the package that is working its way through Congress now with infrastructure and a Green New Deal. And these are going to be serious economic consequences if we see our folks in D.C. continue to act this imprudently.

When we think about the inflation numbers, something to keep in mind is we have seen a boom in housing prices. And a lot of people have enjoyed their home equity going up, but they’re finding that when they look to get a bigger home—they have a few kids, look for a bigger home—they’re finding the price out of the marketplace.

Same goes for people that are looking to buy their first house. They’re realizing, “Wow, these housing costs are out of control.” A lot of people are being forced to rent longer term.

Of interesting note, that big rise in house prices doesn’t even factor into these inflation numbers. And that’s because the inflation numbers basically estimate what people are typically paying in rent and rent costs have been rising, but at a more subdued rate than other items. And now that these leases are beginning to expire, and now that landlords are beginning to recognize that there’s a risk of eviction moratoriums being continued or possibly happening in the future, there’s a good chance that these rental prices are going to be increasing at a faster clip over the next year, which may also end up impacting overall inflation.

Blair: Wow. … That definitely seems like a really strong consequence of this that we should be focusing on, for sure. That was Joel Griffith, a research fellow in The Heritage Foundation’s Roe Institute for Economic Policy. Joel, thanks again for joining us.

Griffith: Thanks for having me.

Have an opinion about this article? To sound off, please email [email protected] and we’ll consider publishing your edited remarks in our regular “We Hear You” feature. Remember to include the URL or headline of the article plus your name and town and/or state.

Read the first chapter of The Woketopus right now for FREE

Today, even with President Trump’s victory, leftist elites have their tentacles in every aspect of our government.

The Daily Signal’s own Tyler O’Neil exposes this leftist cabal in his new book, The Woketopus: The Dark Money Cabal Manipulating the Federal Government.

In this book, O’Neil reveals how the Left’s NGO apparatus pursues its woke agenda, maneuvering like an octopus by circumventing Congress and entrenching its interests in the federal government.

You can read the first chapter of this new book for FREE in this eBook, The Woketopus: Chapter One using the secure link below.

TRENDING ARTICLES

The Daily Signal depends on the support of readers like you.

RELATED ARTICLES

Don’t miss the